Andrew Whitelaw presenting on yesterday’s NSW Farmers webinar.

YESTERDAY’S announcement of a two-week ceasefire between Iran and the US has the potential to reopen shipping through the Strait of Hormuz, and the news prompted an immediate drop in global crude oil prices.

However, no such drop is in sight for urea prices, according to Episode 3 founder and director Andrew Whitelaw speaking yesterday afternoon on the NSW Farmers The Three Fs: Food, Fuel and Fertiliser. What’s ahead for Aussie farmers webinar.

On fuel, improved supply seems likely now the ceasefire is in place, and potential therefore exists for price drops, but the outlook for fertiliser remains clouded as Australian winter croppers enter their peak demand period.

Values for diesel have roughly doubled since conflict broke out on February 28, and urea prices have also skyrocketed.

Flat grain prices worrying

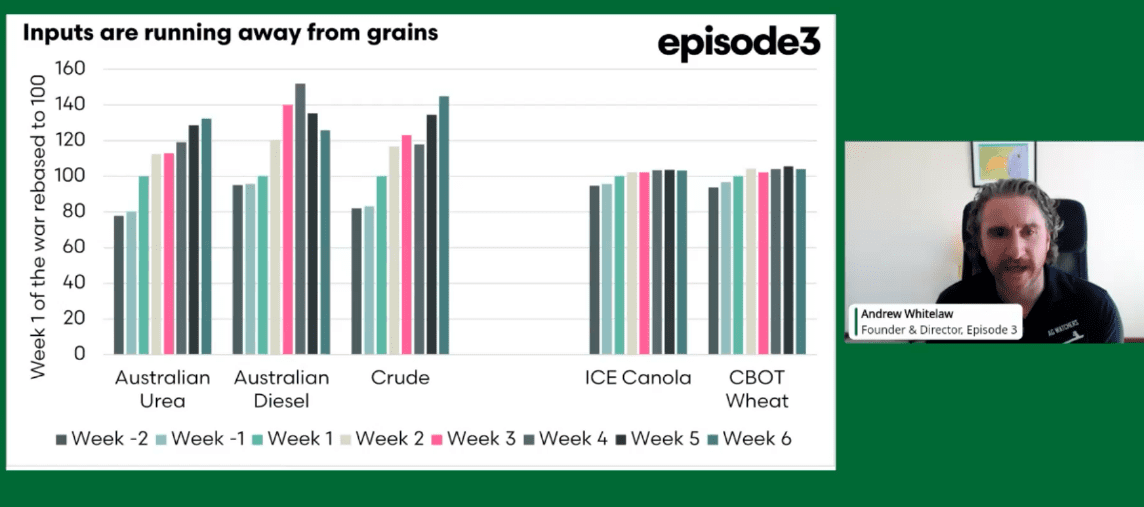

Mr Whitelaw said of greatest concern was the juxtaposition of inflated fuel and urea markets against flat global grain and oilseed markets, as indicated in the image above.

“I put this up on Twitter this morning and I got told it was the most depressing chart that they’d ever seen in their life,” Mr Whitelaw said of the graphic.

“Those markets for inputs have gone up massively, but on the flipside…the dial has hardly moved on our output prices.

“My biggest concern is the timing mismatch.

“We’re paying for all these high inputs, but we probably will not sell the majority of our outputs until December.

Even against the broadside of restricted fuel and fertiliser as a result of the Strait of Hormuz being closed, global markets as indicated by ICE canola and CBOT wheat values have barely moved under the weight of huge oilseed and grain stocks.

“We’ve paid out for a lot of expensive inputs so there’s no guarantee we can recoup those.”

Brighter on fuel

No-one would argue with Mr Whitelaw’s summation of Australian diesel pricing as having “gone absolutely bonkers”, as indicated by the terminal-gate price of around $1.60 per litre in late February to its peak of $3.20 since.

While news of the Iran-US ceasefire is undoubtedly positive, its impact is part of a “changeable and volatile situation”, with global crude oil markets dropping by around 20pc in the few hours following yesterday’s announcement.

Mr Whitelaw said a narrowing of the diesel-to-crude oil spread may bring some relief.

It sat at around 75 cents per litre from 2004-2022, but widened once Australia got down to only two refineries.

“After refineries closed down, that spread has increased rapidly to a record level.”

“It’s now more than $2, but should come down.”

“Diesel’s not actually been the top of our concerns for Australia…unless it extended into May-June onwards.”

He said Asian refiners had supplies for March-April production, and some of that has come to Australia following a “big month of diesel imports in January”, and February being above average also.

Figures show Australia imported 22 percent more diesel in Q1 2026 than it did in Q1 2025, and Mr Whitelaw said April diesel imports, either discharged or on the water, amounted to 88pc of the April 2025 volume.

“New boats are getting added every day pretty much and it seems to me that they’re increasing their flow on what they’d typically do.”

He said fuel was also coming into Australia from atypical origins, including “a couple of boats” from the US, and one tanker from the UK, now heading south off the west coast of Africa.

“The ceasefire is here so they’ll be more boats moving.”

Urea scarce, expensive

Mr Whitelaw said the outlook on urea was not as promising in terms of either increased supply or softening prices.

Provided the Strait of Hormuz can reopen safely, he said urea stocks in the Middle East to come out of Persian Gulf ports can be loaded straight away, but shutdowns and damage to facilities means production cannot resume immediately.

“Restarting those facilities, that is a two-week job.”

“The one that we are most concerned about is urea; unfortunately, it’s not a lot of good news.”

Source: episode 3

Mr Whitelaw said indications are that 16-20pc of Australia’s annual urea requirement could be in the country or on its way as we head into our peak import months.

“June is where we get the bulk of our imports; April-May are big months for imports.

“What happens if it doesn’t come in in time for that top-dressing period?”

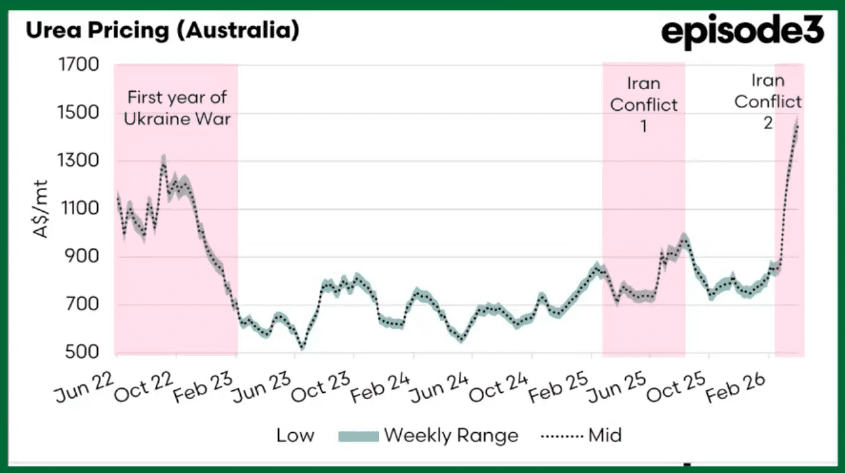

While urea prices went from around $700/t to $900/t during last year’s short-lived Iran-US conflict with Iran, Mr Whitelaw said they are now “just shy of $1500/t landed at port”.

“This conflict is a lot bigger than that conflict, and now we’re seeing levels that have exceeded that of the first year of the Ukrainian war.”

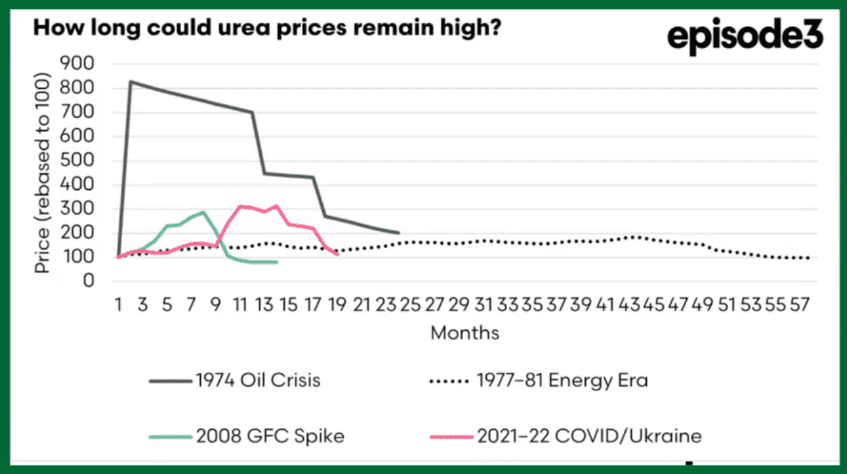

Mr Whitelaw said the question now was around how long urea prices will hold up.

Based on four periods of price spikes as shown below, he said the “tail” of inflated pricing was generally about 19 months, with the 1977-1981 period being the longest.

Source: episode 3

In contrast to Western Australia, Mr Whitelaw said force majeure is not believed to have been called with regard to urea contracts in eastern or South Australia.

However, he advised growers to get a written contract on any fertiliser booked rather than relying on verbal agreement, and said if suppliers can get urea, they are obliged to, regardless of the price.

“It’s still up to the seller to prove that they couldn’t buy it from elsewhere…even if it costs them more money.”

Grain Central: Get our free news straight to your inbox – Click here